posted

Probably one of the best stocks for 2c that has an actual plan to growing and surviving this rout in the mining sector. Information from their last financial report below.

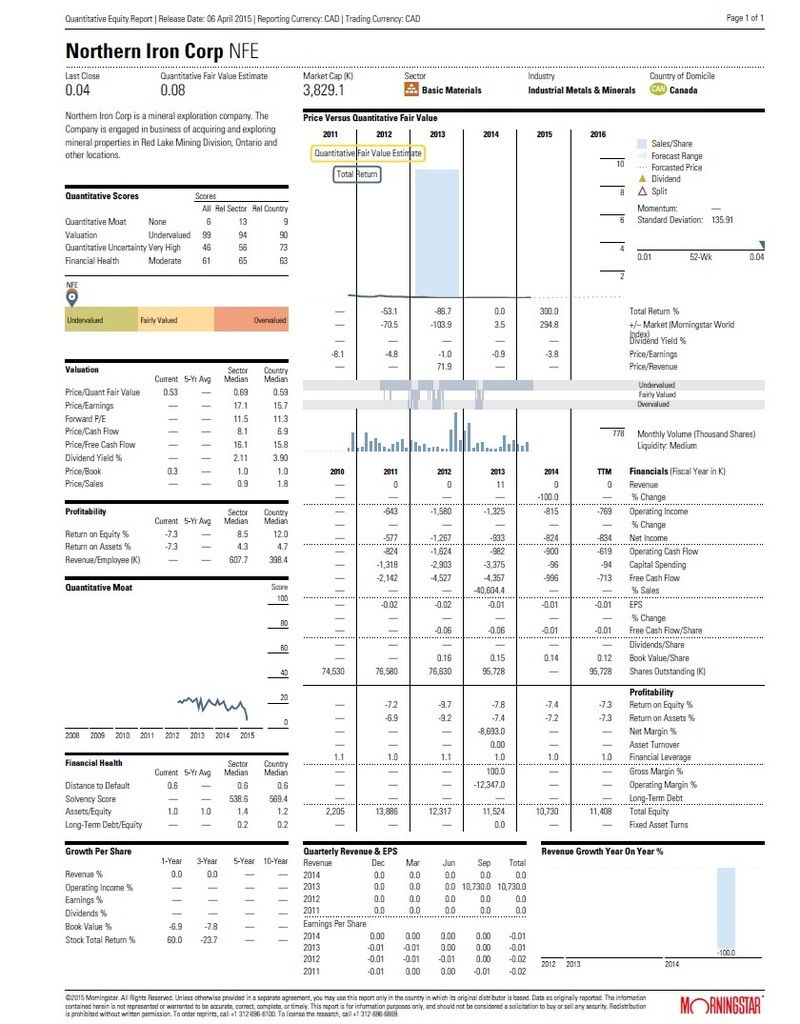

Symbol: NFE Price: $0.02 Shares Outstanding: 95,727,875 common shares (recent placement included) Insider Holdings: Just under 25% as per www.sedi.ca March 2015 Presentation on their website: http://www.northernironcorp.com/

NFE Financials(Most Recent Out Ending June 30th 2014)

Cash: $829,258 ($952,400 raised in December at $0.05c a share, 3 times the current price) Receivable: $84,785 Prepaid Expenses: $4,385 Deposits: $205,264 Intangible Assets: $145 Property and Equipment: $350,740 Exploration Assets: $9,573,315 Total Assets: $11,047,892 (Without PP funds)

Liabilities/Debt: $59,270(All Payables)

Quarterly cash burn: $188,313 for 3 months or $563,953 after 9 months. Roughly $200k per quarter

- $952,400 raised at 5c a share by one individual who is now a director/insider - More financing offered to get this NFEs Iron Ore project into production - Company has three contracts signed that's slated for production deliverance in 2016

News Highlight: Basil Botha, president and chief executive officer of Northern Iron, said: "The investment agreement entered into today is significant for the following reasons:

"The private placement is being done at a 152-per-cent premium to the 20-day volume-weighted average price of Northern Iron shares. "The initial tranche of capital from the private placement, when completed, is expected to secure Northern Iron's short-term working capital needs. "The $30.2-million in further capital provided for in the underlying agreements to be entered into on closing is expected to bring the project to the completion of the bankable feasibility study stage. "These transactions provide Northern Iron with a clear path forward at a time when financing for juniors is extremely difficult. "Northern Iron is now aligned with Danieli Centro Metallics, one of the world's leading equipment suppliers to the steel industry (see press release dated May 7, 2014, regarding co-operation agreement with Danieli), and with OMC, a firm that has access to major Chinese steel producers. "Globally, steel mills are looking for a reliable source of value-added raw materials that can assist in the production of quality and speciality steels, while reducing emissions, being more energy efficient and producing less waste. Canadian HBI [hot briquetted iron] produced in Northern Ontario can accomplish this and the transportation infrastructure is in place to make it happen."

-------------------- Top picks: Visionstate - VIS Fintect - FTEC East West - EW

IP: Logged |

posted

NORTHERN IRON CORP. NOTICE OF ANNUAL AND SPECIAL MEETING OF SHAREHOLDERS NOTICE IS HEREBY GIVEN that an annual and special meeting (the Meeting) of the holders of the common shares (collectively, the Shareholders or individually, a Shareholder) of Northern Iron Corp. (the Corporation) will be held at 409 Granville Street, Suite 1001,Vancouver, BC, V6C 1T2 on Friday, April 10, 2015 at the hour of 3:30 PM, local time for the following purposes: 1. to receive the audited financial statements of the Corporation for the financial year ended September 30, 2014, together with the report of the auditor thereon; 2. to elect the directors of the Corporation to hold office for the ensuing year; 3. to appoint MNP LLP, Chartered Accountants, as auditor of the Corporation for the ensuing year and to authorize the directors of the Corporation to fix its remuneration; 4. to consider and, if thought appropriate, pass, with or without variation, a resolution approving the Corporations rolling stock option plan, as more fully described in the accompanying management information circular dated March 6th, 2015 (the Circular); 5. to consider, and if thought appropriate, pass, with or without variation, a resolution to confirm, ratify and approve By-law No. 1B as adopted by the Corporations board of directors to amend the Corporations by-laws to decrease the quorum requirement for meetings of Shareholders from 25% of the issued common shares of the Corporation entitled to vote at any such meeting to 15%, as more fully described in the Circular; and 6. to transact such other business as may properly be brought before the meeting or any adjournment for adjournments thereof.

A Shareholder wishing to be represented by proxy at the Meeting or any adjournment thereof must deposit his, her or its duly executed form of proxy with the Corporations transfer agent and registrar, Equity Financial Trust Company, by mail or by hand at 200 University Avenue, Suite 300, Toronto, Ontario, M5H 4H1, by fax at 1-416-595-9593 on or before 3:30 PM on Wednesday, April 8, 2015 or deliver it to the Chairman of the Meeting on the day of the Meeting or any adjournment thereof prior to the time of voting. Shareholders who are unable to be present personally at the Meeting are urged to sign, date and return the enclosed form of proxy in the envelope provided for that purpose. If you plan to be present personally at the Meeting, you are requested to bring the enclosed form of proxy for identification. The record date for the determination of those Shareholders entitled to receive the Notice of Annual General Meeting of Shareholders and to vote at the Meeting was the close of business on March 6, 2015. DATED at Toronto, Ontario this 6 th day of March, 2015. BY ORDER OF THE BOARD Basil Botha Basil Botha President and Chief Executive Officer

-------------------- Top picks: Visionstate - VIS Fintect - FTEC East West - EW

IP: Logged |

posted

Northern Iron hires RPA for Karas resource estimate

2015-03-24 04:08 MT - News Release

Mr. Basil Botha reports

NORTHERN IRON CORP. RETAINS RPA INC. TO COMPLETE MINERAL RESOURCE ESTIMATE AND NI-43-101 TECHNICAL REPORT ON THE KARAS PROPERTY

Northern Iron Corp. has retained RPA Inc. to prepare an initial mineral resource estimate and supporting National Instrument 43-101 technical report on the Karas project located near Red Lake, Ont. Basil Botha, President and CEO, commented: "The Karas property is approximately thirteen kilometers east of the past producing Griffith Mine and is considered an excellent supplemental supply source to the project moving forward. The combination of the Griffith and Karas projects provide an adequate feedstock to ultimately produce hot briquetted iron for the North American steel market."

RPA is a group of technical professionals who have provided advice to the mining industry for nearly 30 years. During this time, RPA has grown into a highly respected organization regarded as the specialty firm of choice for resource and reserve work. RPA provides services to the mining industry at all stages of project development from exploration and resource evaluation through scoping, prefeasibility and feasibility studies, financing, permitting, construction, operation, closure and rehabilitation. RPA's portfolio of customers includes clients in banking (both debt and equity), institutional investors, government, major mining companies, exploration and development firms, law firms, individual investors, and private equity ventures."

Toby Hughes, P. Geo., is the Qualified Person for Northern Iron Corporation under NI 43-101.

posted

From the March 2015 presentation is states that management has 3.8% of the 96 million shares, OMC has 20% of them and the institutions below have another 3.44%

Targeted Security Holder Results - 6 items Name Shares Held % of OS Report Date Change ALPHANORTH RESOURCE FUND 2,430,303 3.17 20140630 new COLLEGE RETIREMENT EQUITIES FUND-STOCK ACCOUNT ^ 205,853 0.27 20130331 new IG AGF CANADIAN DIVERSIFIED GROWTH FUND 0 0.00 20130930 -441,172 AGF ALL WORLD TAX ADVANTAGE GROUP-CANADIAN GROWTH EQUITY CLASS 0 0.00 20130930 -1,321,462 SHORT POSITIONS 0 0.00 20140315 -100,000 MARQUEST EXPLORER SERIES FUND 0 0.00 20140630 -3,939,394 Holdings of Fund/Holder COLLEGE RETIREMENT EQUITIES FUND-STOCK ACCOUNT ^ Address: 730 THIRD AVENUE, NEW YORK, NY, USA, 10017 Total Value at last report: $ 118,269,904,000 USD Total number of securities: 526

Holdings of Fund/Holder ALPHANORTH RESOURCE FUND Address: 144 FRONT STREET WEST, SUITE 420, TORONTO, ON, CANADA, M5J 3L7 Total Value at last report: $ 2,954,000 CAD Total number of securities: 19

Below is a current list from SEDI:

Issuer Name: Northern Iron Corp.

Date of Last Reported Transaction(YYYY-MM-DD) Security Designation Registered Holder Closing Balance Insider's calculated balance Closing balance of equivalent number or value of underlying securities

Insider Name: Botha, Basil

Insider Relationship: 4 - Director of Issuer

Ceased to be Insider: Not Applicable

2014-12-10 Common Shares

1,024,500

2014-02-28 Options (Common Shares)

950,000

950,000

Insider Name: Brown, David Richard

Insider Relationship: 4 - Director of Issuer, 5 - Senior Officer of Issuer

Ceased to be Insider: Not Applicable

2012-03-20 Common Shares

525,000

2011-08-18 Options (Common Shares)

350,000

350,000

Insider Name: Carvalho, Felipe

Insider Relationship: 4 - Director of Issuer, 6 - Director or Senior Officer of 10% Security Holder

Ceased to be Insider: Not Applicable

2014-11-28 Common Shares OMC Investments Limited 19,048,000

posted

NFE.V Vs RXM.C(Two Ontario Hot Briquetted Iron ore Companies Beside Each Other) NFE is located North West of Dryden Ontario, RXM is North East of Dryden Ontario. Comparison has been taken from both recent financial reports, presentations and other company information. Recent private placements have also been included below. NFE raised 19 million shares at 5 cents in December for $952,000 while RXM raised $125,000 at 2 cents in December. NFE.V RXM.C Current Price $0.03 $0.065 Common Shares 95.8 million 103.7 million Cash $1.28 Million $150,000 Total Assets $11.5 Million $18.3 Million Liabilities/Debt $54,000 $362,000 NFE March 2015 Presentation: http://media.wix.com/ugd/f57d32_f89af32d59f54d6db5689a9c91021e13.pdf RXM 2015 Presentation: http://www.rockexmining.com/i/pdf/Corporate-Overview-Consolidated-2pg.pdf RXM has a more detailed cost per tonne breakdown compared to NFE, but because these deposits are so similar in proximity an grade, I would say NFE will also be able to produce a tonne of Iron at under $40. This is an amazing cost considering the industry is suffering at a current 6 year low of $54USD per tonne. Converted to Canadian dollars, this is almost $65CDN which makes is much more economical for both companies. Now although RXM has most exploration assets compared to NFE, they have just over 1/10th the cash position and had to raise it at 2c compared to 5 cents with NFE. Without cash its very hard to keep the company afloat, let alone move it forward. Then the big kicker is here are the partners involved. RXMs last news release talks about the company trying to find a partner for its project. Well NFE has them beat by a long shot because Northern Iron not only has a financing partner, they also have three buyers lined up to purchase the Hot Briquetted Iron they produce. OMC Investments(Hong Kong) have already invested $1 million dollars and will put up to $30 million to get everything operational for 2016. There are 3 buyers in place for the HBI and its a total of 1.46 million tonnes. At a current price of around $250USD per tonne, thats quite the accomplishment. On page 4 of their Griffith Assessment : http://media.wix.com/ugd/f57d32_713095fdaa6247dfa0bb0c111976a122.pdf

NIC=Northern Iron Corp. NFE is the ticker symbol.

NIC has negotiated an off-take agreement with the China Railway Materials Import and Export Company (900,000 metric tonnes of HBI annually to be delivered commencing in 2016). This order represents about two thirds of the annual production of HBI from the Griffith Mine. NIC has also negotiated an off-take agreement with Tianjin Materials & Equipment Group Corporation of China for 60,000 metric tonnes of HBI to be delivered annually starting in 2016. The rest of the production will be offered for sale to the world market. China Railway Material - 900,000 Tonnes Tianjin Materials - 60,000 Tonnes Danieli - 500,000 Tonnes

The Danieli deal was not announced until mid-2014.

So after comparing the two companies, its easy to see that NFE has farther along and likely to go into production well before RXM. So why is it trading so low? The answer to that is exposure. Its mixed in with lots of 2-3 cent mining/exploration stocks that are ready to go bust due to lack of funds. A current fair price for NFE would be around the 8 to 10 cent range. Any additional funding from OMC is not going to dilute the stock, rather it has been setup in a sidecar company which will take interests in the assets and not dilute Northern Irons common stock.

-------------------- Top picks: Visionstate - VIS Fintect - FTEC East West - EW

IP: Logged |

posted

AGM Info sheet and April 2015 presentation. No rollback mentioned and it's because we don't need it going forward. Company will be funded without dilution.

Some good information on how the deal will work going forward:

On December 1, 2014, the Corporation announced the closing of a private placement and joint venture announced on October 16, 2014, with OMC Investments Limited, of Hong Kong (OMC). Pursuant to the terms of an investment agreement between the Corporation and OMC (the Investment Agreement), the Corporation issued 19,048,000 units to OMC (each, a Unit) by way of private placement at a price of $0.05 per Unit, for aggregate gross proceeds of $952,400 (the Private Placement). Each Unit consisted of one Common Share and one Common Share purchase warrant, with each warrant (Warrant) being exercisable by OMC for a period of three years from the closing of the Private Placement at a price of $0.05 per Common Share. Pursuant to the terms of the Investment Agreement, OMC was entitled to nominate one individual for approval as a director of the Corporation to take effect immediately following the closing of the Private Placement (the OMC Nominee). Accordingly, on December 1, 2014, Felipe Carvalho, was appointed to the Board of the Corporation as the OMC Nominee with immediate effect. As disclosed below under - 12 - the heading Election of Directors, Mr. Carvalho has been nominated at the Meeting for election as a director of the Corporation. If Mr. Carvalho is elected at the Meeting, he will continue to act as the OMC Nominee. In connection with the closing of the Private Placement, the Corporation incorporated three subsidiaries under the Business Corporations Act (Ontario), namely Canadian Iron Metallics Inc. (CIM), Griffith Iron Metallics Inc. (GIM) and Karas Iron Metallics Inc. (KIM). In addition, in connection with the Private Placement, the Corporation received the consent of the Ministry of Northern Development and Mines to transfer its (i) 23 unpatented contiguous mining claims comprising the Griffith property (the Griffith Claims) to GIM, and (ii) 21 unpatented contiguous mining claims comprising the Karas property (the Karas Claims) to KIM. Northern Irons remaining unpatented mining claims relating to its El Sol property, Papaonga property and Whitemud property remain in the name of the Corporation. Concurrent with the Closing of the Private Placement, and subject to the terms of a subscription agreement between the Corporation and an affiliate of OMC (the Affiliate), the Affiliate subscribed for 15% of the common shares in the capital of CIM, with the Corporation holding the remaining 85%. The Corporation and the Affiliate, as shareholders of CIM, also entered into a shareholders agreement (the Shareholders Agreement) in order to address, among other matters, the organization and affairs of CIM, the funding of key developmental steps in relation to the Griffith Claims and the Karas Claims, and the sale of shares of CIM. Also in connection with the Private Placement, the Corporation entered into an option agreement with OMC (the Option Agreement) pursuant to which, subject to certain conditions, OMC or an affiliate thereof has (i) the right to acquire up to 80% of the issued and outstanding shares of a wholly-owned subsidiary of the Corporation (the Subsidiary) to be incorporated by the Corporation to hold the mineral rights comprising the Companys El Sol property, Whitemud property or Papaonga property if and only if OMC funds the entirety of an $8.2 million resource delineation work program in connection with the Corporations Griffith Claims and Karas Claims (the 80% Interest), and (ii) if OMC earns the 80% interest, the further right to increase its interest in the Subsidiary to 90% of the issued and outstanding shares if, within the five year period during which OMC earns the 80% Interest, OMC funds an additional $1.5 million of exploration work on such property. Other than the foregoing, no informed person (as such term is defined in NI 51-102) or proposed nominee for election as a director of the Corporation or any associate or affiliate of the foregoing has any material interest, direct or indirect, in any transaction in which the Corporation has participated since the commencement of the Corporations most recently completed financial year or in any proposed transaction which has materially affected or could materially affect the Corporation.

-------------------- Top picks: Visionstate - VIS Fintect - FTEC East West - EW

IP: Logged |

posted

Northern Iron completes magnetic survey at Griffith

2015-04-07 04:11 MT - News Release

Mr. Basil Botha reports

NORTHERN IRON CORP. COMPLETES MAGNETIC SURVEY AND WATER SAMPLING PROGRAM ON THE GRIFFITH MINE PIT

Northern Iron Corp. has completed a magnetic survey and water sampling program on the Griffith mine pit.

The magnetic survey comprised 14 lines over approximately two-thirds of the north pit. The survey resulted in a large volume of raw data which, once analyzed, will allow the company to plan and execute a drill program, once the pit has been partially dewatered.

An integral part of the expected drill program is the requirement to dewater. The water sampling program provided the raw data required to complete the company's submission of a permit to dewater an additional 15 metres below the 25-metre dewatering permit previously issued by the Ministry of Environment.

Basil Botha, president and chief executive officer, commented: "This time of the year allowed us to deploy a two-man crew to complete the magnetic survey over the frozen pit and auger a hole through the ice to take a series of water samples at various levels. When one considers the value of the datasets collected, the work programs are low cost and the data invaluable. The water samples will assist us in our submission of the second dewatering application for an additional 15 metres, allowing the company to dewater a total of 40 metres. Gaining access deeper into the pit will expose the benches in the southern part of the pit on which to begin a drill program."

Composite Indicators Signal Get Chart Get Performance TrendSpotter Buy

Short Term Indicators Get Chart Get Performance 7 Day Average Directional Indicator Buy Get Chart Get Performance 10 - 8 Day Moving Average Hilo Channel Buy Get Chart Get Performance 20 Day Moving Average vs Price Buy Get Chart Get Performance 20 - 50 Day MACD Oscillator Buy Get Chart Get Performance 20 Day Bollinger Bands® Hold

Short Term Indicators Average: 80% Buy 20-Day Average Volume - 91,589

Medium Term Indicators Get Chart Get Performance 40 Day Commodity Channel Index Hold Get Chart Get Performance 50 Day Moving Average vs Price Buy Get Chart Get Performance 20 - 100 Day MACD Oscillator Buy Get Chart Get Performance 50 Day Parabolic Time/Price Buy

Medium Term Indicators Average: 75% Buy 50-Day Average Volume - 93,726

Long Term Indicators Get Chart Get Performance 60 Day Commodity Channel Index Hold Get Chart Get Performance 100 Day Moving Average vs Price Buy Get Chart Get Performance 50 - 100 Day MACD Oscillator Buy

Long Term Indicators Average: 67% Buy 100-Day Average Volume - 152,791

Overall Average: 80% Buy

Price Support Pivot Point Resistance 0.030 0.030 0.030 0.030

-------------------- Top picks: Visionstate - VIS Fintect - FTEC East West - EW

IP: Logged |

New video from NFE's ceo explaining the difference between typical Iron ore and DRI/HBI. This will help set the record straight that NFE is still in a very lucrative business compared to the loses mounting on standard iron ore production. On top of that, NFE is in a safe jurisdiction compared to the rest of the other HBI producers worldwide(Libya, Venezuela, etc).

As well, great news today from US Steel Business. Looks like prices are starting to rise and this is a bullish. Article link below:

posted

News release just now, RXM is working with Danieli(who is also NFE's partner) to develope their HBI mine which is not far from NFE's Griffith Mine. This means the HBI industry is actually moving forward and that's a positive sign! Only difference is that RXM has no money compared to NFE ($1.1 million vs $70k) and they don't have an investment partner like OMC. So if RXM is worth 2 cents a share as is, then NFE should be at 5-6 cents right now. Read the news below:

Rockex to work with Danieli to develop Eagle Island 2015-06-29 14:56 MT - News Release

Mr. Armando Plastino reports ROCKEX MINING SIGNS CO-OPERATION AGREEMENT WITH DANIELI FOR PROJECT DEVELOPMENT INITIATIVES FOR ITS 100% OWNED EAGLE ISLAND PROJECT Rockex Mining Corp. has signed a co-operation agreement with Danieli & C. Officine Meccaniche SpA of Buttrino (Udine), Italy, for the two parties to co-operate and collaborate to develop Rockex's 100-per-cent-owned Eagle Island iron ore deposit near Sioux Look-Out in Northwestern Ontario. The agreement contemplates the development of an integrated operation comprising a concentration plant, a pelletizing plant, an Energiron direct reduction plant and related auxiliary systems, all of which would be designed to ultimately produce 4.0 million tonnes per year of hot briquetted iron ("HBI"). The first stage of the co-operation effort establishes Danieli as a technological partner for marketing and promoting the Eagle Island project to possible strategic partners, financiers and final product off-takers that can support Rockex's efforts and expenses for the preparation of a bankable feasibility study. The agreement has an initial term of two years and, on achieving certain milestones, will automatically extend for an additional two years. If a positive bankable feasibility study is completed and certain levels of financing and off-take commitments are achieved, the agreement contemplates that Danieli and Rockex will negotiate in good faith a cost-competitive definitive agreement for Danieli to supply the concentration plant, the pelletizing plant and the direct reduction plant. If the parties are unable to settle the terms of such an agreement or if Rockex sells Eagle Island without Danieli's ongoing participation then, in certain circumstances, Rockex will be obligated to pay a break fee to Danieli. "We are very excited about the support and confidence that Danieli has shown in Rockex and our Eagle Island project," said Armando Plastino, Chief Executive Officer of Rockex. "Danieli is a large multi-national engineering firm with an excellent reputation and extensive experience in designing and constructing plants like the ones we will need at Eagle Island. I believe that their willingness to support our efforts at this early stage in exchange for the opportunity to negotiate a cost-competitive agreement speaks volumes for their belief in the ultimate success of Rockex's Eagle Island project." In the latter half of 2013, Rockex received a National Instrument 43-101 compliant report (the "Report") summarizing the results of a formal Preliminary Economic Assessment (the "PEA"). This Report was prepared by Met-Chem Canada Inc. ("Met-Chem") for the Eagle Island project. The results of the PEA were first announced by Rockex in a comprehensive news release issued on August 27, 2013. Both the PEA and the initial news release can be viewed on Rockex' SEDAR site at www.sedar.com and Rockex' own website at www.rockexmining.com. Rockex is in the process of revising the 2013 PEA to include HBI as the final product. In this regard, a contract to upgrade the PEA to include HBI has been awarded to CIMA+, Engineering Consultants. A draft version of the revised PEA is expected by the end of July, 2015. Highlights of the 2013 PEA include:

$ 3.9 Billion Net Present Value with a 5% discount rate (pre-tax) $ 2.2 Billion Net Present Value with an 8% discount rate (pre-tax) 20.7% Internal Rate of Return (pre-tax) dot 4.2 year pay back Initial Investment of $1.559 billion (not including sustaining capital of $609 million) Average site operating cost of $36.63/tonne of iron concentrate (pellet feed) Updated Resource Estimate doubling Eagle Island's Indicated Mineral Resource to 1.287 billion tonnes at 28.39% iron plus an Inferred Mineral Resource of 108 million tonnes at 31.03% iron. Life of Mine Production of 6 million tonnes of 66.3% iron concentrate per year for 30 years. Low strip ratio of 0.51 to 1

Summary of the 2013 PEA The PEA is based on the production of 6 million tonnes of iron concentrate (pellet feed) per year at a grade of 66.3% total iron ("Fe"). The average run of mine feed of 17.3 million tonnes per year used is based on a mill recovery of 80% operating year-round from the Eagle Island deposit. The life of mine of 30 years was based on 512 million tonnes of in-pit resources at a grade of 28.9% Fe. This tonnage is less than half of Eagle Island's estimated Indicated Resources of 1,287 million tonnes at a grade of 28.39% Fe. Initial capital expenditures are estimated at $1.559 billion for the production of 6 million tonnes per year of iron concentrate (pellet feed). Using an average site operating cost of $36.63 per tonne, and assuming the iron concentrate (pellet feed) sales price at $105USD FOB Sioux Lookout, calculated Net Present Value for the Eagle Island project is $3.9 billion (pre-tax) using a 5% discount rate and $2.2 billion (pre-tax) using an 8% discount rate. In addition to the PEA, Rockex completed an updated independent Mineral Resource estimate by Met-Chem which has defined 1,287 million tonnes of Indicated Resources at a grade of 28.39% Fe and 108 million tonnes of Inferred Resources at a grade of 31.03% Fe. The updated resource is summarized in the Table below.

Mineral Resource Category Metric Tonnes (Millions) Fe (%) Indicated 1,287 28.39 Inferred 108 31.03

Northern Iron Corp seeks partner to develop DRI project in Canada

July 21, 2015

Canada-based Northern Iron Corp is looking for a strategic partner to develop a direct reduction iron (DRI) project in the city of Dryden, in the countrys east-central Ontario province.

"We aim to find a US steel mill interested in securing [DRI] supply," corporate development vp Michael Hepworth told Steel First.

The company intends to develop a 1.5 million-tpy DRI operation in Canada, but a detailed project will be designed only after the conclusion of a pre-feasibility study, expected next year.

Completion of this study depends on funding, however.

Northern Iron Corp will use the Griffith mines iron ore reserves, estimated at 125 million tonnes, to feed the DRI plant. The mine, also located in Dryden, was operated by a local firm from 1968 to 1986.

With the project, the company aims to benefit from the growing demand for DRI in the US market.

About 60% of the steel in the USA is currently produced via electric arc furnaces (EAF), according to Northern Iron Corp.

"Prime scrap [material] is scarce and the quality of other scrap types is declining, however," Hepworth said. "And EAFs cant use iron ore, only metallics [such as DRI]."

The reduced volumes of hot briquetted iron (HBI) produced by Venezuelan firms could also boost demand for Northern Iron Corps DRI output, he said.

Besides targeting the US market, the company has already signed a take-or-pay offtake agreement with Italy-based Danieli Centro Metallics.

Under the deal, it will supply 500,000 tpy of DRI to the European firm.

Danieli Centro Metallics is a global technology provider, in sectors from iron ore processing up to DRI production, including EAF feed.

Meanwhile, Northern Iron Corp is betting on its proximity to the US steel industry and easy access to Asian and European markets to foster the development of the DRI project in Canada.

From Dryden, the DRI would be transported by rail to the existing Canadian ports of Thunder Bay and Prince Rupert for export.

"We would have to buy shipping capacities at these terminals [to export]," Hepworth said.

The miner would also take advantage of cheap and regular long-term access to clean natural gas in the region, which would reduce its energy costs by 10%.

A natural gas line already exists at Northern Iron Corps mining property, according to the company.

Northern Iron Corp is not connected to the similarly named Australian mining company, Northern Iron.

NORTHERN IRON CORP. COMPLETES MAGNETIC SURVEY ON THE GRIFFITH PIT

Northern Iron Corp. has completed approximately 11 line kilometres of ground magnetic surveys on the Griffith property.

The survey successfully outlined the broad trend of the iron formations within the North Griffith pit. Depth estimates to mineralization and precise widths were not made. The data provide a guide to the next phase of drilling.

A total of 10.99 line kilometres of ground magnetic surveys were completed using a GSM-19 Version 7 Overhauser magnetometer system.

Magnetic readings were downloaded daily and corrected with the base station data.

Readings were taken every 20 metres along 100-metre-spaced traverses originally set at 118-degree orientation. Portions of some lines, in particular at their eastern extremities, could not be surveyed due to the slope of the pit. The survey outlined the main iron formation previously partially extracted, and reveals the main north-northeast-to-northeast (folded) trend. The southern continuation of the mineralized body is seen extending off pit; the anticlinal sequence is observed as a broader expression, and the east limb, trending south to southeast appears as a near-vertical sequence in the southeast corner of the pit and grid. Correlation with the geology indicates a steep westerly dip for the main iron formation. Overall increase in magnetic intensity to the south is a function of the approximate 35-degree plunge of the iron formation and possibly higher-grade material. The syncline-anticline-syncline geometry is imprecisely defined, due to said plunge, partial extraction of the north portion of the fold set, and possibly to previously unknown faulting by east-southeast-trending discontinuities. The data provide a guide to the next phase of drilling, much of which would be contingent on the dewatering of the pit. A partial dewatering of the pit would provide reasonable access for in-pit delineation drilling of the main iron formation, with collars on the D bench (level).

Drilling on bench D, about 100 m vertically below datum, would test the southern extension of the main iron formation both along strike and down plunge. All holes would be drilled downdip, but drilling from the west would not be as cost-effective due to the layout of the benches.

Drilling of the south extension outside of the pit would be easily achieved, using pre-existing roads, although the extent of flooding in the area should be assessed.

Similarly, there should be some additional testing of the east limb, in the far southeast corner of the pit.

It is vital to test the south extension and down-plunge continuity of the major folded iron formation in the centre south of the pit. For this reason, it is necessary to dewater the pit past level F. Some surface drilling could commence whilst the pit is dewatered. The continuity of the iron formation, based on the recent survey, provides reasonably accurate definition of the target. Also, drilling at this stage would provide some estimates of grade and width to at least near-surface iron content. It is stressed that such intercepts may not be representative of anticipated higher grades at depth.

Further, the results from any subsequent drilling will have an impact of future pit geometry, and it is conceivable that an alternative to significant aerial pit expansion would be access south by a broad ramp, eliminating the need to expand benches B and C, and possibly D. Estimating costs associated with the proposed drilling is contingent on locations on particular bench levels and hence total lengths of individual drill holes. In-pit drilling would benefit from pads on E rather than D benches, reducing several drill hole lengths by up to 100 metres. Strike extensions to the south should be targeted based on the results of the in-pit drilling.

The technical information in the news release has been prepared in accordance with Canadian regulatory requirements set out in National Instrument 43-101 and reviewed on behalf of the company by its qualified person, Paul Sarjeant, PGeo (Ont.), qualified person has prepared, supervised the preparation of approved the scientific and technical disclosure in the news release.

Northern Iron is a mineral exploration company focused on developing high quality iron ore opportunities in the Red Lake Mining Division of Ontario, Canada, which is a past-producing iron ore district. The Company is a 100% owner of five iron ore properties in the Red Lake district containing significant historical resources with grades ranging from 22% to 31% Fe2O3. Northern Iron is listed on the TSX Venture Exchange and commenced trading on 26 August 2011.

The resource definition drilling program at the Griffith Mine commenced in August of 2012 and 11 holes totaling 3730m were completed by 21 September 2012. The holes were drilled around the perimeter of the North Pit. Past production indicated the higher grades and larger resource are located towards the South end of the pit. This should be the priority area for delineation drilling. It is estimated that a minimum of 10,000 meters will be required on the south-west and north-east. Fence drilling can be carried out from the East side, and fan drilling farther South.

For the Company to continue to operate as a going concern it must continue to obtain additional financing to maintain operations; although the Company has been successful in the past at raising funds, there can be no assurance that this will continue in the future. In an effort to preserve capital, the Company has ceased all field activity and deep cost cutting measures have been adopted. In addition to the reduction in field work, these cost cutting measures include significant reductions in consulting, travel, and shareholder relation expenditures. At the current burn rate the Company has sufficient cash reserves until mid-2016. There were additional cost cutting measures that came about in May 2014 that will provide the Company with additional cash into January 2017.

The Company is focusing the majority of its efforts in introducing the Griffith mine project to prospective industry partners in North America. It is the intention of management to attract a large industry partner into the project to provide expertise and capital to advance the project.

-------------------- Top picks: Visionstate - VIS Fintect - FTEC East West - EW

IP: Logged |

UBBFriend: Email this page to someone!

UBBFriend: Email this page to someone!

Printer-friendly view of this topic

Printer-friendly view of this topic